What a perpetual, leverage and margin actually are

A perpetual contract (or perpetual future) is a derivative that lets you speculate on an asset's price without owning it, and unlike traditional futures it has no expiry, so you can hold it as long as you keep enough margin. That last clause is the whole game.

Leverage is widely sold as buying power: 10x means you control ten times the position for the same money. That framing is true and misleading at once. The honest definition is the mirror image: leverage is how thin your loss buffer is. At 10x, a 10% move against you wipes out your entire margin. At 100x, a 1% move does. Leverage does not change where the market goes or your expected return from the trade. It changes only how small a move it takes to close you out.

Margin is the collateral backing the position, and it comes in two flavours that matter here. Initial margin is what you need to open a position; on ApeX Omni it is Position Size x Entry Price x the initial margin rate (ApeX docs). Maintenance margin is the smaller amount you must keep to hold the position open: Position Size x Mark Price x the maintenance margin rate. When your equity falls to that maintenance margin - the point ApeX Omni measures as a margin ratio of 100% - liquidation triggers. The gap between what you posted and that maintenance floor is your entire margin for error.

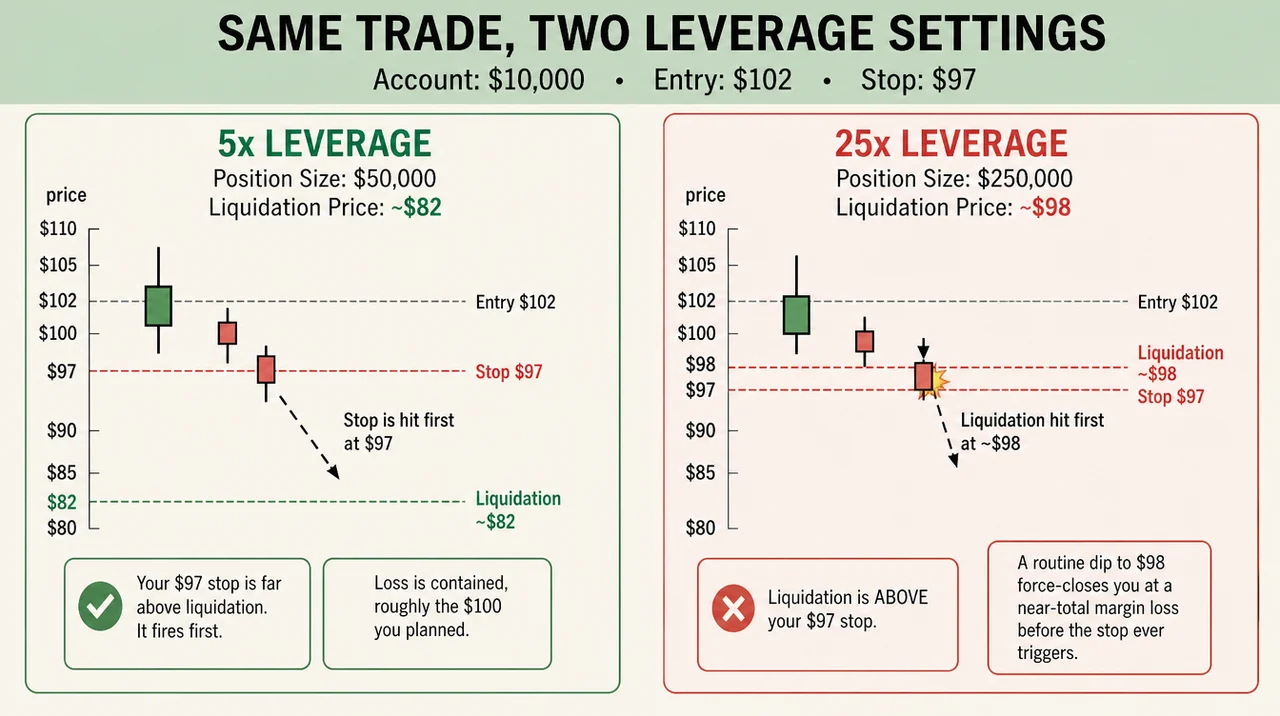

Watch a liquidation happen

Take the exact trade from the previous part: a $10,000 account, a long entered near $102, with the structural stop at $97. Unleveraged, that is a five-point risk, and a sensible size loses about $100 if the stop hits. Now put it on as a perp and watch leverage move the liquidation line. (These use an illustrative maintenance margin rate of about 0.5%; real rates vary by pair and size, and in cross margin your other positions shift the maths too.)

Same chart, same correct read, same stop, opposite outcome, driven entirely by the leverage dial. At 5x the instrument respected your plan. At 25x the liquidation price jumped inside your stop and the trade was decided by margin mechanics, not by whether you were right about the level. This is the discontinuity the earlier "just set a stop" lesson hid: on a leveraged perp, your first job is to check that your liquidation price is beyond your stop, not the other way round. The fix is simple - lower the leverage until it is.

Why "high leverage means high returns" is the costliest myth in trading

Leverage amplifies a winning trade, and that is exactly why it is dangerous: it amplifies the losing trade and the liquidation probability by the identical factor, and most trades are not clean winners. The evidence on leveraged retail trading is some of the least ambiguous in finance.

When the European regulator ESMA studied the industry before restricting it in 2018, its data across national authorities found that 74% to 89% of retail accounts typically lose money, with average losses per client ranging from €1,600 to €29,000 (ESMA, 2018). The UK's FCA reached the same neighbourhood independently: its analysis of a representative sample of CFD client accounts found 82% of clients lost money (FCA, 2016).

Here is the detail worth sitting with. ESMA did not just warn about leverage; it capped it, limiting retail crypto exposure to 2:1 and major currencies to 30:1. A perpetuals DEX may offer up to 100x. The regulators who looked hardest at leveraged retail trading concluded the safe retail ceiling for crypto was two times, not one hundred. That gap is not a coincidence, and it is not the exchange being generous. It is the difference between what is available and what is survivable.

Why you were "liquidated on a wick" (and why that is the system working)

The most common liquidation complaint is that the price never actually reached the liquidation level - a single candle wick stabbed down, closed you out, and recovered a second later. It feels like theft, or a stop hunt. Usually it is neither, and the reason is worth understanding because it protects you.

Liquidations on a well-built perpetuals venue are not triggered by the last traded price on that one exchange. They are triggered by a mark price, a fair-value estimate deliberately smoothed against manipulation. On ApeX Omni the mark price is the median of a funding-adjusted index, a basis-adjusted index, and the last price, where the index itself is a weighted average of spot prices from several major exchanges (ApeX docs). A wick on a single venue's order book barely moves that median. ApeX's own documentation answers the complaint directly: "Liquidation only occurs when the Mark Price reaches the liquidation threshold, protecting you from temporary spikes."

So a real liquidation on mark price means the aggregated, cross-exchange fair value genuinely hit your level, not that one venue printed a bad tick. The mechanism you are cursing is the one stopping a manipulated wick on some other exchange from closing you. That does not mean stop hunts are a myth - price genuinely gravitates toward clusters of stops and liquidation levels, because that is where the resting liquidity is. But "the market moved to where the orders were" is a liquidity phenomenon, not a personal attack, and index-based mark pricing is specifically what stops it from being manipulation.

One honest footnote on the data you will see quoted around these events: headline liquidation totals are undercounts. Since April 2021, Binance's public liquidation feed pushes at most one liquidation per second, so during a cascade, when thousands fire at once, the reported figure is a floor, not the true total. When a crash is described as "billions liquidated," the real number was larger.

Cross margin: the catch that raises your liquidation price on trades you were winning

ApeX Omni runs one margin model: cross margin, where all positions share a single pool of equity. The upside is capital efficiency and that a winning position's unrealised profit cushions a losing one. The catch, which the docs state plainly, is contagion: a large loss on one position drains the shared equity and pushes every other position closer to liquidation. Your liquidation price is not a fixed property of one trade; it drifts as the rest of your book moves. Add a second losing position and the first one's liquidation price climbs toward the market, even if that first trade was fine on its own.

And liquidation is not always a clean exit at the liquidation price. The clearing engine closes underwater positions at the best available market price, and if that still leaves a shortfall, it is absorbed by the auto-deleveraging system, which can close part of a profitable trader's opposing position to cover the gap. The realised damage can exceed the tidy number a liquidation-price calculator shows you.

Reputation versus evidence

Claim: "High leverage means high returns"

What is taught: Leverage multiplies your gains.

What actually happens: Leverage multiplies gains, losses, and the probability of liquidation equally. The European Securities and Markets Authority (ESMA) found that 74–89% of retail accounts lose money, leading it to cap retail crypto leverage at 2:1.

Claim: "My stop-loss protects me"

What is taught: Your stop-loss caps the loss at your chosen invalidation level.

What actually happens: At high leverage, the liquidation price can sit inside your stop-loss level, causing your position to be liquidated with a near-total loss of margin before the stop-loss is ever triggered.

Claim: "I was liquidated on a wick"

What is taught: The exchange hunted my stop.

What actually happens: Liquidation is based on the mark price, which is derived from a cross-exchange price index. A sharp wick on a single exchange usually has little effect on the mark price, so liquidation mechanisms are generally operating as designed rather than targeting individual traders.

Claim: "More collateral makes me safe"

What is taught: Adding more funds removes liquidation risk.

What actually happens: Adding collateral increases the distance to liquidation but never eliminates the risk. In cross margin mode, losses from one position also reduce the available margin protecting every other open position.

Claim: "Liquidation is a clean exit"

What is taught: You only lose the difference between your entry and liquidation price.

What actually happens: Liquidation is a forced closure at the best available market price and typically includes a liquidation fee. If the position cannot be closed at the bankruptcy price, any remaining shortfall may be handled through mechanisms such as auto-deleveraging, meaning losses can extend beyond the expected liquidation outcome.

Trading with leverage without getting burned

Check your liquidation price before you confirm, every time - it is displayed before you open. If it sits inside your intended stop, your leverage is too high for this trade. Lower it until the liquidation price is safely beyond the stop.

Treat leverage as a liquidation-distance dial, not a size dial - the question is never "how big can I go" but "how far can price move against me before I am closed."

Keep your margin ratio well below 100% - ApeX Omni liquidates the instant it reaches 100%, and experienced traders generally keep theirs below 50% to 60% under normal conditions.

Remember cross margin is shared - size your whole book, not each trade in isolation, because a loss anywhere pulls every liquidation price closer.

Cut leverage before known volatility - funding events, major data releases, and thin weekend liquidity are when the wick that reaches mark price actually happens.

Common mistakes

Setting the stop and ignoring the liquidation price - the stop is useless if the liquidation price is nearer. Check both, and make the stop the closer of the two.

Reading leverage as free size - 100x is not a hundred times the opportunity, it is also one hundredth of the room to be wrong.

Blaming the wick - if you were closed on mark price, the cross-exchange fair value hit your level. The lesson is lower leverage, not a conspiracy.

Forgetting the shared pool - opening a second leveraged position quietly raises the liquidation price on the first.

Liquidation on ApeX Omni

Because ApeX Omni is a perpetuals DEX, this is not abstract theory - it is the product. Before you open a position, the platform shows your estimated liquidation price and your live margin ratio, so the two numbers this article is about are on screen at the moment of decision. Liquidations run on the manipulation-resistant mark price rather than a single wick, the account uses cross margin so your whole equity backs every position, and full contract specifications, including the maintenance margin rate for each pair, are published so you can compute your own buffer. The honest way to use all of it is the boring way: modest leverage, a liquidation price comfortably beyond your stop, and a margin ratio you never let creep toward 100%. Read the full Margin, Risk Management and Liquidations guide, then check your own liquidation price on ApeX Omni before your next trade.

The bottom line

Leverage is not a return multiplier, it is a survival dial. It leaves your expected outcome unchanged and simply decides how little room you have to be wrong before the liquidation price closes you - a price that, turned up high enough, sits inside the very stop you set to protect yourself. The regulators who studied leveraged retail trading most closely found the large majority lose money and capped retail crypto leverage at two times for a reason. Use leverage the way the evidence argues for: sparingly, with your liquidation price checked against your stop before every trade, and with a margin ratio you keep far from the edge. Being right about the chart is only half of it. The other half is making sure the instrument does not close you before your read gets the chance to be right.

Frequently asked questions

What is a liquidation price? The price at which your position is force-closed because your equity can no longer cover the maintenance margin. On ApeX Omni it is calculated on the mark price and depends on your leverage, your margin, and, in cross margin, your other positions.

Can I be liquidated before my stop-loss triggers? Yes. At high leverage your liquidation price can sit closer to the entry than your stop, so it fires first and closes you at a near-total margin loss. Always check that your liquidation price is beyond your stop.

Why was I liquidated when the price on the chart never hit my liquidation level? Because liquidations use the mark price, a fair value drawn from a cross-exchange index, not the last traded price on one venue. A temporary wick on the chart does not move the mark price enough to liquidate you; only the aggregated fair value reaching your level does.

Does higher leverage increase my expected profit? No. Leverage scales both profit and loss by the same factor and raises your probability of liquidation; it does not change the trade's expected return. Regulators found 74% to 89% of retail leveraged accounts lose money.

Does adding more margin stop me from being liquidated? It widens your buffer and pushes the liquidation price further away, but it never removes the risk. In cross margin, a loss on any position reduces the buffer protecting all of them.

What is the safest leverage to use? There is no single number, but the direction is clear: lower is safer. Set leverage so your liquidation price sits well beyond your stop, and keep your margin ratio well below 100%.

Explore more from this series: Part 8: Putting It All Together | Part 10: Funding Rates - Coming Soon

This article is for educational and informational purposes only and is not financial, investment, or legal advice. Do your own research before making any trading decision.