What a funding rate actually is

A perpetual contract never expires, which is the feature that makes it convenient and the feature that creates a problem. A dated future is dragged toward the spot price by its expiry: on settlement day, the two must meet. A perpetual has no settlement day, so something else has to keep its price from drifting away from the underlying market. That something is the funding rate.

Funding is a periodic payment exchanged directly between long and short position holders, and its purpose is to anchor the perpetual price to spot (ApeX docs). The direction is simple. When the perpetual trades above spot, the rate is positive and longs pay shorts, which discourages longs and pulls the price back down. When it trades below spot, the rate is negative and shorts pay longs. The exchange is not the counterparty and does not pocket the payment; it moves between traders. On ApeX Omni the platform even caps the hourly rate and absorbs any excess itself, rather than passing it on.

The mechanism is not new to crypto. The idea of a never-expiring futures contract balanced by a funding payment traces to the economist Robert Shiller, who described perpetual futures in a 1993 paper, and it reached crypto when BitMEX launched the perpetual swap in 2016 (BitMEX). Nearly every crypto perp you can trade today is a descendant of that design.

Watch funding drain a winning trade

Funding is abstract until you put a position value on it. Take a live snapshot from ApeX Omni: a 5 BTC long, a BTC index price of about $64,174, and the current funding rate, roughly +0.0006% per hour (0.00000582). Funding is quoted and settled every hour, so treat this as one reading, not a fixed number.

FUNDING ON A 5 BTC LONG (index ~$64,174, current funding +0.0006% per hour)

position value: 5 x $64,174 = ~$320,870

one hour: 320,870 x 0.00000582 = ~1.87 USDT paid to shorts

one day (ApeX settles hourly): ~45 USDT, about 0.014% of the position

held flat for a week: ~314 USDT, price unchanged

worst case at the +0.05%/hr cap: ~3,850 USDT a day, over 1% of the positionThat $1.87 is the funding fee for a single hour, computed as Position Size x Index Price x Funding Rate. Funding is calm as this is written: ApeX Omni settles every hour, so at the current rate the long pays only about 45 USDT a day, roughly 0.014% of the position, and a little over 300 USDT across a flat week. But the rate is not fixed. It swings with positioning, and ApeX Omni caps it at 0.05% per hour, close to a hundred times the current level. At that ceiling the same 5 BTC long bleeds about 3,850 USDT a day, over 1% of the position, or more than 400% annualised. The lesson holds right across that range. If you are long through persistently positive funding, your directional read has to beat the funding drag, not just break even on price. A correct call that goes sideways can still be a losing trade.

Note the interval, because it trips people up. Most exchanges settle funding every eight hours; ApeX Omni settles every hour. The per-payment number is therefore smaller on ApeX, but it arrives more often, and only positions open at the exact settlement timestamp pay or receive. The figure that matters is the daily and weekly drag, not any single tick.

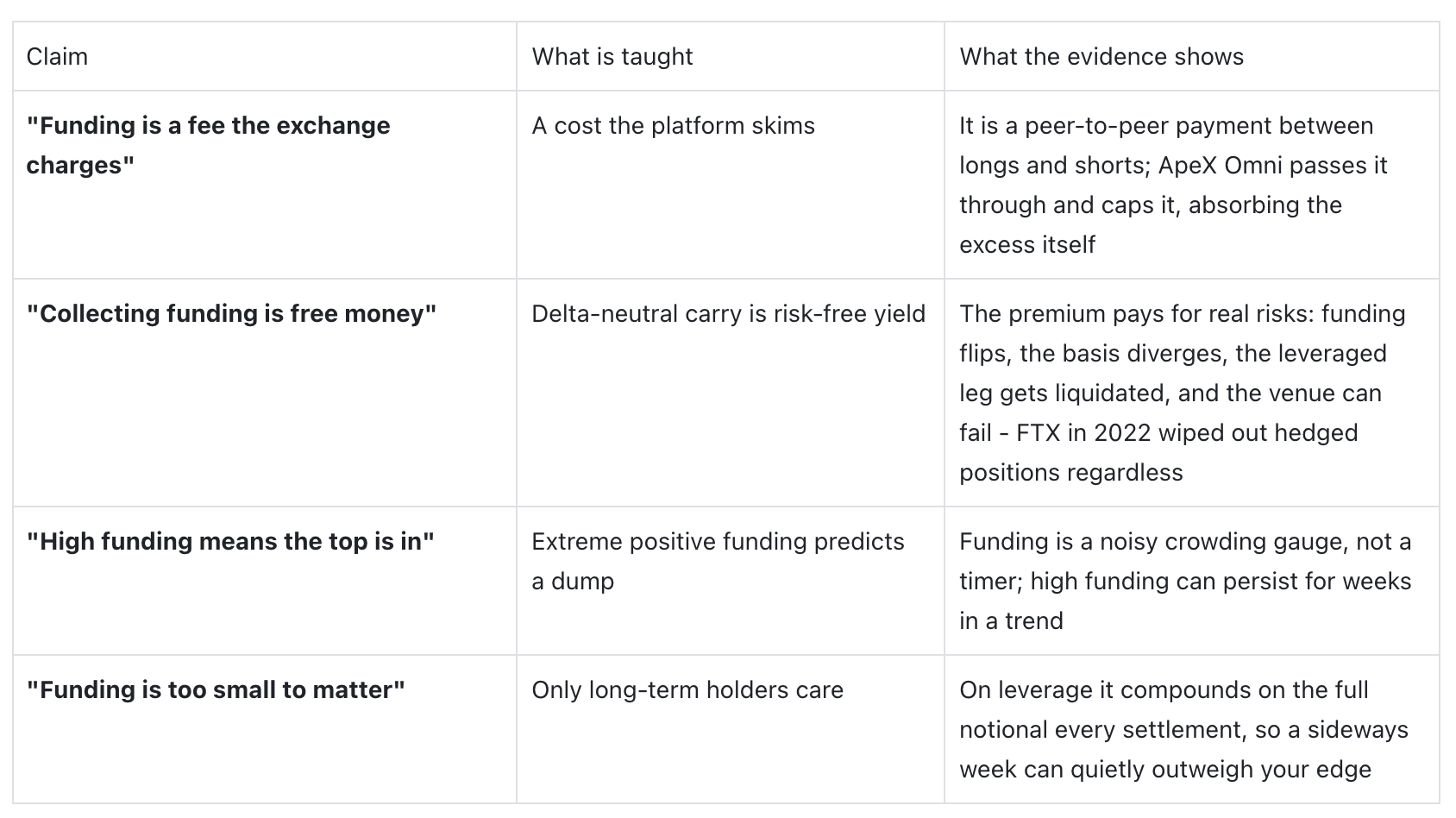

Is collecting funding really free money?

Because funding is usually positive in a bull market, with longs paying shorts most of the time, a strategy suggests itself: take the payment without the price risk. Buy the asset on the spot market and simultaneously short the same size on the perpetual. Your price exposure cancels out - if BTC falls, your spot loss is offset by your short's gain - and you sit there collecting the funding the longs pay. This is the cash-and-carry, or basis trade, and delta-neutral funding farming is marketed everywhere as passive, near risk-free yield, with advertised returns from single digits in calm markets to triple-digit annualised figures in frothy ones.

The mechanism is real. The framing is the most dangerous folklore in perps. A persistent positive funding rate is not a gift the market leaves lying around; it is compensation for risks that are quiet until they are not.

Funding can reverse. The rate that made the trade attractive can flip negative in a downturn, so the position you opened to collect funding starts paying it instead.

The basis can diverge. Spot and perp do not track perfectly; the gap can widen against you faster than the funding compensates, and low-funding periods can see costs exceed the funding collected.

The hedge is leveraged. The short-perp leg usually uses leverage, so a sharp rally can liquidate it, breaking the neutrality and turning a "market-neutral" trade into a directional loss at the worst moment.

The venue itself can fail. This is the one that turns "delta-neutral" into "everything, gone." When FTX collapsed in November 2022 with an estimated $8 billion shortfall in customer funds, it did not matter whether your positions on the exchange were perfectly hedged (FTX bankruptcy). Your spot and your short were both on a platform that no longer had the money. The carry trade's real counterparty was never the other trader; it was the exchange holding your collateral.

None of this means the carry never works. Peer-reviewed analysis of funding-rate arbitrage finds it can be genuinely profitable, while also documenting that leverage raises rebalancing and trading costs and that the return comes with real drawdown risk (Exploring Risk and Return Profiles of Funding Rate Arbitrage, 2025). The honest summary is the same one this series keeps arriving at: the yield is real, and it is a payment for bearing risk, not a free lunch. Anyone who calls it risk-free has simply not met the risk yet.

Funding as a sentiment gauge, used honestly

Because funding reflects which side is paying to hold leverage, it is a genuine window into positioning. Strongly positive funding means longs are crowded and paying up to stay long; strongly negative means the crowd is short. Extreme readings flag a leveraged, one-sided market, which is exactly the setup that fuels the liquidation cascades from the previous part.

The folklore takes this one step too far: "funding is at record highs, so the top is in, short it." That is where the evidence pushes back. High funding signals crowding, not timing. It can persist for weeks in a strong trend, paying out the whole way up, and squeezing anyone who shorted it on the level alone. Treat funding as a gauge of how crowded and leveraged a move is, a reason to size down and mind your liquidation price, not as a countdown timer to a reversal.

Reputation versus evidence

Trading with funding in mind

Check the funding rate before you hold, not after. A position you would happily hold for a day at zero funding can be a slow loss at high positive funding. It is a cost of carry, so price it in.

Remember funding is charged on notional, not margin. At 10x, your funding bill is ten times the size your margin might suggest, because it is levied on the whole position value.

Do not fade a trend on funding alone. High funding is a reason to lower leverage and respect the squeeze risk, not a standalone short signal.

Common mistakes

Ignoring the drift on a leveraged long - the funding on a big notional can eat a correct read that moves sideways.

Believing "delta-neutral" means "risk-free" - it removes price risk, not funding-reversal, liquidation, or exchange-failure risk.

Shorting extreme funding as a top signal - crowding is not timing, and the trend can pay longs for weeks.

Forgetting the settlement timestamp - only positions open at settlement pay or receive, so the timing of your entry and exit around it changes the bill.

Funding on ApeX Omni

Because ApeX Omni is a perpetuals DEX, funding is a live cost you can read before you commit. It settles hourly, on the hour in UTC, as a peer-to-peer payment between longs and shorts, with the rate computed from an interest-rate and premium-index component and capped at plus or minus 0.05% per hour, and the funding fee is levied on your position value at the index price. Only positions open at the settlement timestamp pay or receive. The practical takeaway is the same as everywhere in this series: know your funding before you hold, size for it on leverage, and never confuse a yield with a free one. Read the full Trading and Funding Fees guide, and check the live funding rate on ApeX Omni before your next held position.

The bottom line

A funding rate is the tether that keeps a never-expiring contract honest, a small payment passed between longs and shorts to hold the perp near spot. It is not the exchange's fee, and it is not free money. For a directional trader it is a cost of carry that a correct read still has to overcome; for a carry farmer it is a yield that pays for risks, counterparty failure chief among them, that stay invisible right up until they take everything. Read it as what it is: a live gauge of crowding and a real cost of time in the trade. Price it in, and it stops being the leak that quietly sinks trades you got right.

Frequently asked questions

What is a funding rate in crypto? A periodic payment exchanged directly between long and short holders of a perpetual contract to keep its price aligned with spot. Positive funding means longs pay shorts; negative means shorts pay longs. The exchange does not keep it.

Does the exchange take the funding fee? No. Funding is peer-to-peer between traders. On ApeX Omni the platform passes it through and even caps the hourly rate at plus or minus 0.05%, absorbing any excess rather than charging it.

How often is funding charged? It varies by venue. Most exchanges settle every eight hours; ApeX Omni settles every hour, and only positions open at the exact settlement timestamp pay or receive.

Is funding rate arbitrage (delta-neutral farming) risk-free? No. It removes directional price risk, but funding can reverse, the basis can diverge, the leveraged leg can be liquidated. The yield is compensation for those risks.

Does a high funding rate mean the price will drop? Not reliably. High funding signals crowded, leveraged positioning and elevated squeeze risk, but it can persist for weeks in a strong trend. It is a sentiment gauge, not a timing signal.

How do I calculate the funding I will pay? Funding fee = position size x index price x funding rate, applied at each settlement. On leverage, remember it is charged on the full position value, not on your margin.

Explore more from this series: Part 8: Putting It All Together | Part 9: Leverage and Liquidation | Part 11: Mark, Index and Basis - Coming Soon

This article is for educational and informational purposes only and is not financial, investment, or legal advice. Do your own research before making any trading decision.